Call Now: 954-554-5103

Most Popular Supplement Plans

To choose the right Supplement Plan for you, it is best to compare the 10 standardized Medigap Plans (Plan A, B, C, D, F, G, K, L, M, and N). Each Plan covers different gaps in Original Medicare and each Plan has a different monthly premium cost. It is important to weigh those two factors, and choose a plan that’s best for your health and financial situation. This decision is not easy, but we are here to help you through it! To start, below is a chart which compares all 10 Medicare Supplement Plans.

Most Popular Supplement Plan

As of 2020, the most popular Supplement Plan that our clients choose is Medigap Plan G (otherwise known as Supplement Plan G). What is the reason for this? Well, Plan G is currently the most comprehensive Supplement Plan available to people who are newly eligible to Medicare as of 2020. It has great coverage at a reasonable monthly premium cost. It covers all of the gaps in Original Medicare, except for the Part B annual deductible of $198. It pays for your coinsurance, copays and hospital deductible amongst other benefits. This means that besides this deductible, you should not have to pay out of pocket for any other medical or hospital bills. Also, Plan G has a reasonable monthly premium cost. The average Supplement Plan G premium cost is between $100-$130 per month (the rate varies based on your zip code, age, tobacco usage, and other factors). This is a fairly low cost, considering you will have full medical and hospital insurance, if you add this plan onto your Original Medicare.

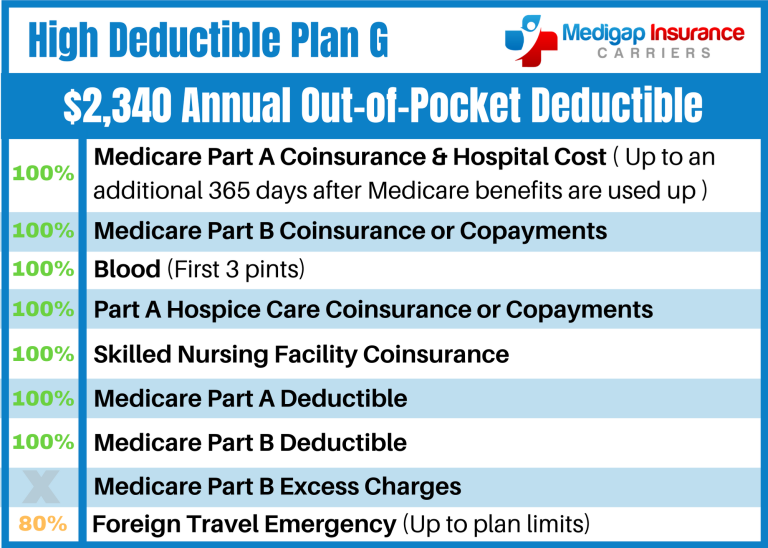

What is covered under Medigap Plan G:

Medicare Part A coinsurance and hospital costs (Up to an additional 365 days after Medicare benefits are used)

Medicare Part B coinsurance or copayment

Blood (First 3 pints)

Part A Hospice care coinsurance or copayment

Skilled nursing facility care coinsurance

Medicare Part A deductible

Medicare Part B excess charges

Foreign travel emergency (Up to plan limits)

What is not covered under Medigap Plan G:Medicare Part B deductible

Other Popular Supplement Plans

Another fairly popular Medigap option is Supplement Plan N. This Plan provides coverage for many of the gaps in Original Medicare, except for the Part B deductible and Part B excess charges. Excess charges are health care expenses that your Doctor could charge in excess of what Medicare is willing to reimburse. *Also, it’s important to note that Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to a $50 copayment for emergency room visits that don’t result in an inpatient admission. However, the monthly premium cost for Plan N is a bit lower than the cost of the more popular Plan G.

What is covered under Medigap Plan N:

Medicare Part A coinsurance and hospital costs (Up to an additional 365 days after Medicare benefits are used)

Medicare Part B coinsurance or copayment*

Blood (First 3 pints)

Part A Hospice care coinsurance or copayment

Skilled nursing facility care coinsurance

Medicare Part A deductible

Foreign travel emergency (Up to plan limits)

What is not covered under Medigap Plan N:Medicare Part B deductible

Medicare Part B excess charges

Before 2020, the most comprehensive and popular Medicare Supplement Plan was Plan F. Therefore, it’s important to note that as of January 1, 2020 Supplement Plan F will no longer be available to people who are newly eligible for Medicare on or after January 1, 2020. The reason for this change is because Medicare will no longer be allowed to cover the Medicare Part B deductible, which this particular Medigap Plan covered. If you already had this plan prior to January 1, 2020, you are able to keep the plan.

What is covered under Medigap Plan F:

Medicare Part A coinsurance and hospital costs (Up to an additional 365 days after Medicare benefits are used)

Medicare Part B coinsurance or copayment

Blood (First 3 pints)

Part A Hospice care coinsurance or copayment

Skilled nursing facility care coinsurance

Medicare Part A deductible

Medicare Part B deductible

Medicare Part B excess charges

Foreign travel emergency (Up to plan limits)

I chose a Supplement Plan, what’s next?

Once you choose your Supplement Plan, you will need to choose the insurance carrier to get the Supplement through. Supplement Plans are standardized by Medicare, which means no matter which private insurance company/carrier you purchase one of these plans from, it will have the same benefits. For Example, Medigap Plan G with Humana will have the same benefits as Medigap Plan G with Cigna, the only difference may be the monthly premium cost. When choosing the insurance carrier, it is important to compare a few factors:

The monthly premium cost of the Supplement Plan. Again, the supplement benefits are the same no matter which carrier you choose, but the premium cost differs between carriers.

Most carriers have premium rate increases annually to keep up with inflation. It’s important to make sure that the rate increases with the carrier you choose, are reasonable compared to other carriers.

Each carrier has different financial ratings, which are based on the company’s financial health and stability. It is best to choose A-rated carriers.

Need more help from the Medicare Experts?

Our well trained agents are ready to answer questions about your Medicare health insurance, and put together a comprehensive plan to fit your needs. Request more information by any of the 3 ways bellow!

Call Us

866-599-6588

Schedule Appointment

Request

A Quote

Medigap Insurance Carriers is not affiliated or endorsed by the United States Government or the Federal Medicare Program. This is a solicitation of insurance.

An agent/producer may contact you for insurance. Medigap Insurance Carriers is a DBA wholly owned by John Ross Anthony Webb.

©Copyright | Medigapinsurancecarriers 2022. All Right Reserved